Previously, I highlighted some of the so-called ‘reopening trades’ that remain on the JSE (There are still ‘reopening trades’ out there), which included Spur Corporation (SUR).

Spur has now released its interim results for the six months to 31 December 2022, revealing just how well it is doing – and the share price has started responding positively.

Read:

How much more upside may be left?

Spur Corp saw its H1:23 restaurant turnover rise 31.5%, driving group revenue up 35% and doubling profit before tax.

Headline earnings per share (Heps) followed suite, with a 198% rise (comparable Heps was up 81% year on year), which management used to hike its dividend 67%.

The group’s balance sheet remains net cash with no gearing, group cash flows remain strong, and core operating expenses were tightly controlled – and, as far as I can tell, remain below pre-Covid levels (in other words, exiting the pandemic leaner and fitter as a group).

Source: The author

While supply chains are still normalising (though they are far better than before, with the exception perhaps of chicken), the group was probably a net beneficiary of load shedding.

Read:

Struggling to get chicken at your nearest fast food chain?

KFC SA to close some units due to power cuts

A full 95% of its stores run on generators (with running costs of only 0.5% to 2.6%), with inverters, battery and solar setups there too.

Thus, when consumers are load-shed around mealtimes, Spur – being Spur, RocoMamas, Panarottis, John Dory’s, The Hussar Grill, and a couple of other brands – is a viable alternative.

Read: SA’s retail and fast-food giants demand tax relief from government

This is especially true if you have kids (Spur absolutely dominates in the family restaurant market), but also if you are using Uber Eats or Mr D for deliveries.

On this latter point, it was great to see Spur management using virtual kitchen (VK) brands like Just Wingz, Pizza Pug and Bento to generate incremental sales.

These incremental sales leverage the group’s existing store footprint, adding high-margin revenues to existing fixed costs that should cascade down the group’s income statement. Also, I suppose, if any of these VK brands really take off, the group can start to roll out specific restaurants for the brands.

Source: The author

This is all positive, and despite pressure on consumer disposable income, Spur is well-positioned going forward with many levers to pull to extract profitable growth.

But how does the share’s valuation look?

The group’s share’s rolling 10-year average price-earnings (PE) ratio is 176 times. Even compared against one standard deviation below this average, its meagre 11.6 times current PE is low. Exceptionally low.

But the world has changed, the South African environment has become tougher, and interest rates have risen (which should benefit ungeared companies, by the way!).

Perspective

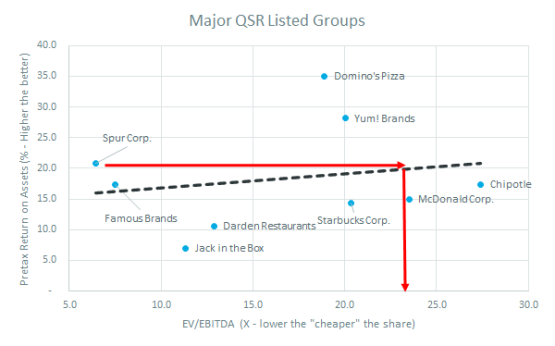

How does Spur stack up against its global peers, and local rival Famous Brands?

Despite being much smaller, Spur (and indeed Famous Brands) compare quite well against major global QSR (quick service restaurants) and normal restaurant chains that are listed.

Both have pre-tax (important to use pre-tax, as other geographies have different tax rates) returns on assets that are higher than most QSR groups.

Interestingly, both are also much cheaper when compared against their EV/Ebitda (enterprise value/earnings before interest, tax, depreciation and amortisation) ratio – which is kind of like a PE ratio, but manages for different cost structures and neutralises different levels of debt to make it more globally comparable.

Now, if we statistically find the ‘line of best fit’ (linear regression) tracking these stocks, the market tends to pay more for QSR stocks that are more profitable. In other words, higher EV multiples on their Ebitda from higher pre-tax returns on assets (ROAs).

Famous Brands is not just less profitable than Spur (lower pre-tax ROA), but its valuation is sitting comfortable on the line of best fit. This implies that Famous Brands is appropriately valued against this peer set.

Opposing this, Spur Corporation’s superior pre-tax ROA implies that it should be materially higher-valued (follow the red line to where its share’s valuation would sit and this implies its EV/Ebitda multiple). In fact, if you follow this logic through, Spur’s valuation (and, hence, its share price) should be a little over two-and-a-half times higher – on an EV/Ebitda approaching 23 times!

Thus, the evidence (greater than a standard deviation undervalued against history and out of kilter with global peers) is that Spur Corp’s shares remain quite comfortably undervalued despite its constructive prospects.

The answer therefore to how much more upside may be left in Spur shares is ‘Could be quite a lot’!

Listen to host Simon Brown and Chantal Marx of FNB Wealth and Investments unpack the trading update issued by Spur Corporation in February:

You can also listen to this podcast on iono.fm here.

* Some of portfolios managed by Integral Asset Management may hold Spur Corp shares.

Keith McLachlan is chief investment officer at Integral Asset Management.