“Stagflation” is an unsightly phrase for an unsightly state of affairs – the disagreeable mixture of financial stagnation and inflation.

The final time the world skilled it was the early Nineteen Seventies, when oil-exporting international locations within the Middle East minimize provides to the United States and different supporters of Israel. The “supply shock” of a four-fold enhance in the price of oil drove up many costs and dampened financial exercise globally.

Stagflation was thought left behind. But now there’s a actual danger of it coming again, warns the central financial institution for the world’s central banks.

“We may be reaching a tipping point, beyond which an inflationary psychology spreads and becomes entrenched,” says the Bank for International Settlements BIS in its newest annual economic report.

By “inflationary psychology” it signifies that expectations of upper costs lead customers to spend now moderately than later, on the belief ready will price extra. This will increase demand, pushing up costs. Thus expectations of inflation turn into a self-fulfilling prophecy.

The hazard of stagflation comes from this inflationary cycle changing into so entrenched that makes an attempt to curb it by means of larger rates of interest push economies into recession.

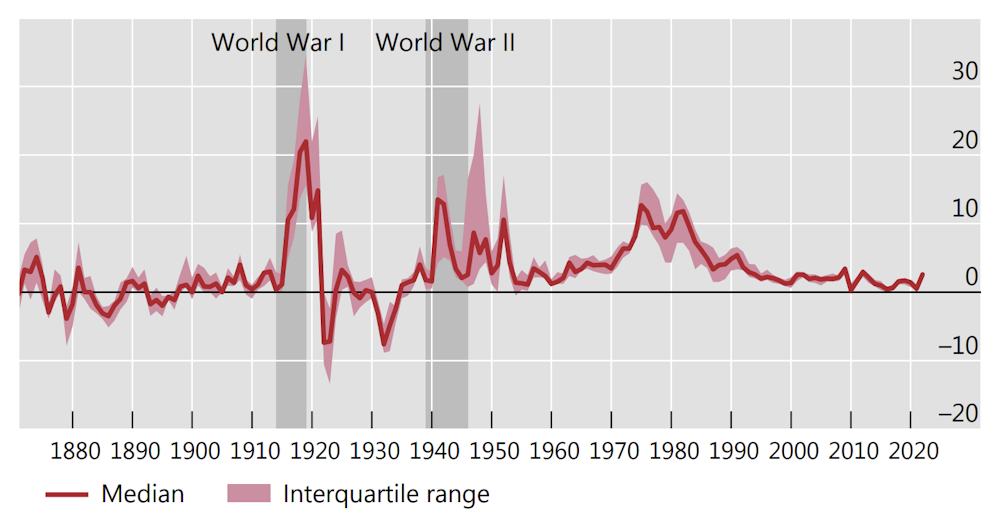

Global inflation because the nineteenth century

{kind=link}

What’s driving inflation

As properly as its personal knowledgeable employees, the BIS brings collectively experience from its member central banks, such because the US Federal Reserve, the European Central Bank, the Bank of England and Reserve Bank of Australia. So its views are value taking note of.

Its report makes clear its consultants, like most forecasters, have been stunned by the extent of the rise in inflation.

This is a worldwide phenomenon, which the report attributes to a mixture of an unexpectedly robust financial rebound from the COVID-19 lockdowns, a sustained swap in demand from providers to items, and provide bottlenecks exacerbated by a shift from “just-in-time” to “just-in-case” stock administration.

Then there’s Russia’s invasion of Ukraine.

Kunihiko Miura/Yomiuri Shimbun/AP

The battle’s impact in driving up the worth of oil, gasoline, meals, fertilisers and different commodities has been “inherently stagflationary”:

Since commodities are a key manufacturing enter, a rise of their price constrains output. At the identical time, hovering commodity costs have boosted inflation in every single place, exacerbating a shift that was already properly in prepare earlier than the onset of the battle.

The solely vivid observe is that BIS expects these worth surges to be much less disruptive than the oil provide shock of the Nineteen Seventies.

This is as a result of the relative influence of the oil provide shock was higher as a consequence of economies within the Nineteen Seventies being extra energy-intensive.

There can be way more focus now on containing inflation, with most central banks having a clearly said inflation goal (2% in Europe and the US, 2%-3% in Australia).

What are the most important risks?

But the present state of affairs remains to be very difficult, the report says, as a result of will increase within the worth of meals and power are notably conducive to spreading inflationary psychology.

This is as a result of meals is purchased incessantly, so worth adjustments are notable. The similar goes for gasoline costs, that are prominently displayed on giant roadside indicators.

There can be the chance in lots of economies of a wage-price spiral – during which larger costs drive calls for for larger wages, which employers then cross on in larger costs.

Central banks face what Reserve Bank of Australia governor Philip Lowe has known as a “narrow path”.

To obtain a “soft landing” they should elevate rates of interest sufficient to deliver inflation down. But not sufficient to trigger a recession (and thus stagflation).

How to keep away from a ‘hard landing’?

The BIS report cites an evaluation of financial tightening cycles – outlined as rate of interest rises in a minimum of three consecutive quarters – in 35 international locations between 1985 and 2018. A mushy touchdown was achieved in solely about half the instances.

A key issue within the arduous landings was the extent of economic vulnerabilities, notably debt. Economies with arduous landings on common had double the expansion in credit score to GDP previous to the interest-rate rises.

This issue contributes to BIS considerations now. As the report notes:

Unlike prior to now, stagflation at this time would happen alongside heightened monetary vulnerabilities, together with stretched asset costs and excessive debt ranges, which might amplify any development slowdown.

Furthermore, the slowdown in China’s labour productiveness is eradicating an essential increase to world financial development and restraint on world inflation.

But a key lesson from the Nineteen Seventies is that the long-term prices of doing nothing outweigh the short-term ache of bringing inflation underneath management.

This means governments should curb handouts or tax cuts to assist folks with cost-of-living pressures. Expansionary fiscal coverage will solely make issues worse. Assistance should be strictly focused to those that most want it.

There can be a have to rebuild financial and financial buffers to deal with future shocks. This would require elevating rates of interest above inflation targets and returning authorities budgets (shut) to surplus.![]()

John Hawkins, Senior Lecturer, Canberra School of Politics, Economics and Society, University of Canberra

This article is republished from The Conversation underneath a Creative Commons license. Read the original article.