What will be the best option for my provident fund when resigning?

[ad_1]

Dear Reader,

Thank you for your query and congratulations in your new job. Firstly let’s clarify what a provident preservation fund is.

A provident preservation fund is a kind of retirement fund that allows people to protect their retirement financial savings on leaving their employer’s provident fund.

The preservation fund has to be regulated by the Pension Funds Act and is related to tax advantages – as such, a provident preservation might solely settle for tax-free transfers from a provident fund or one other provident preservation fund.

As of 1 March 2021, a brand new regulation got here into impact in the Pension Funds Act. New contributions made to provident funds from this date will be topic to the similar necessities as a pension preservation fund or retirement annuity.

For those that have been already members of provident and provident preservation funds on 1 March 2021, all advantages in these funds as at 28 February 2021, plus any future progress on these advantages, will not be impacted by the modifications. These advantages will be given ‘vested rights’, that means that members will nonetheless be in a position to take as much as 100% of those vested advantages in money at retirement. In addition to the vested rights on present advantages as at 28 February 2021, if a provident fund member is 55 or older they will additionally obtain vested rights on the advantages from the new contributions made to those funds from 1 March 2021 onwards. However, the modifications will influence your new contribution made to your new provident fund.

When shifting employers, you might be permitted to maneuver your earlier provident fund to your new employer. However, earlier than making a call, it is very important perceive all the choices accessible to you.

You have mentioned that you just wish to take a money lump sum earlier than transferring the funds into one other provident fund or a provident preservation fund. You are permitted to take any quantity, but it surely will be subjected to the withdrawal lump sum profit tax desk, as proven under.

| Taxable revenue (R) | Rate of tax (R) |

| R1 – 25 000 | 0% |

| R25 001 – 660 000 | 18% of taxable revenue above R25 000 |

| R660 001 – 990 000 | R114 300 + 27% of taxable revenue above R660 000 |

| R990 001 and above | R203 400 + 36% of taxable revenue above R990 000 |

At retirement, people are entitled to R500 000 tax-free. This implies that when you choose to take a sure portion (not larger than one-third of your retirement funds) as a money lump sum, the first R500 000 will be tax-free. Thereafter, the quantity will be taxed as per the retirement lump sum profit tax desk. However, previous to retirement if any withdrawals have been created from a retirement fund, this will influence the R500 000 tax-free quantity.

We suggest that, if you don’t require a money lump sum out of your provident fund, you switch the full portion right into a provident preservation fund to protect the capital.

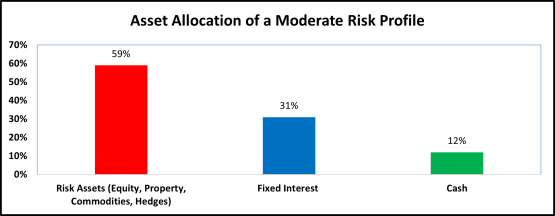

Regarding the danger technique in your preservation fund, we usually suggest that you just think about a reasonable danger technique.

|

Example of a reasonable technique |

||||

| Annualised return | ||||

| Funds | Allocation | 1 12 months | 3 years | 5 years |

| Equity fund | 25% | 13% | 10% | 10% |

| Balanced fund | 25% | 10.75% | 10% | 8% |

| Stable fund | 25% | 7.50% | 8% | 6% |

| Income fund | 25% | 7% | 7% | 8% |

| Weighted common value and return | 100% | 9.56% | 8.75% | 8% |

| Returns are as at 30/11/2022. Past performances usually are not a assured of future returns | ||||

Please be aware a mean return was used for every asset class.

Source: Global & Local

You can anticipate progress of between 8% to 10% every year as proven above.

Your monetary advisor will be in a position you information you to the proper resolution, nevertheless, you might be greater than welcome to contact us.

[ad_2]